Save articles for later

Add articles to your saved list and come back to them any time.

Last weekend, I went out to dinner with some people, most of whom I’d never met before. Upon sharing that I work in financial education, I was met with an enthusiastic array of questions.

The one that always comes up in these scenarios is “how do I start investing?” What many people don’t realise is that good investing starts long before you invest the money.

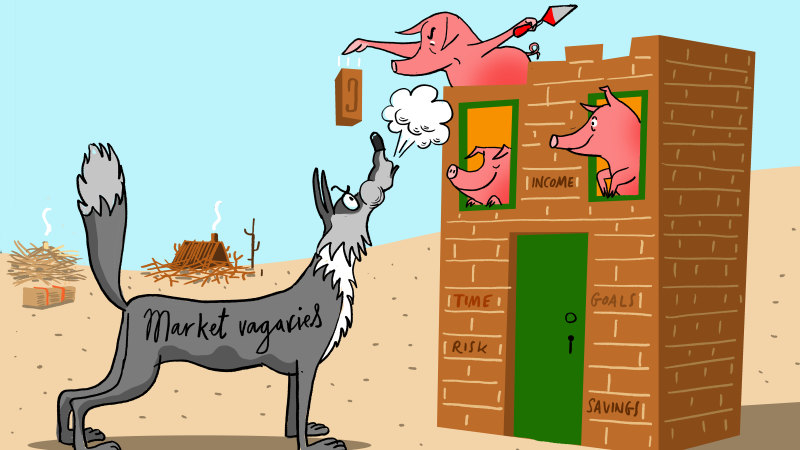

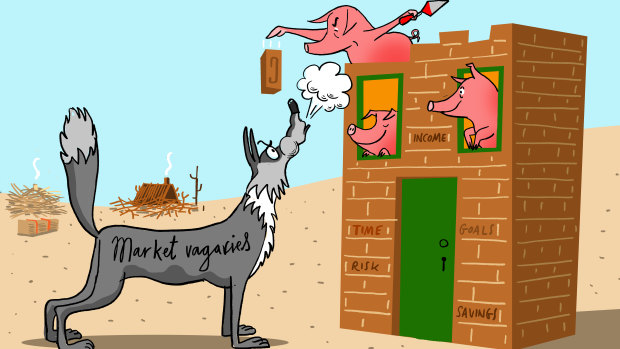

Investing is a bit like building a house. There’s a lot of planning that goes on before you lay the first brick.Credit: Simon Letch

If you really want to set yourself up for investing success, the part you should focus on is the preparation you need to do.

It’s a bit like building a house. There’s a lot of planning that goes on before you lay the first brick. In fact, building should be the simplest part if you’ve done the preparation well.

Investing isn’t something you should rush into out of a fear of missing out. There is some preparation you can do to make your investment journey more fruitful in the long term.

As part of the preparation process, here are some things you should consider:

Investing doesn’t start with opening a brokerage account and buying an investment.

1. Do you have high-interest consumer debt? Let’s say you have an interest rate of 17 per cent on your credit card, and you have a debt that you carry on that card which you’re paying interest on.

Historically, on average, the stock market has delivered a 7-10 per cent return over the long term.

So if you invest money and think you’re going to make a return while you still have high-interest credit card debt, you’ll actually be losing money faster than you’re making it.

If you have high-interest debts, one of the best things you can do to lay a stronger foundation for your future investments is to prioritise paying them down as fast as possible.

2. Do you have an emergency fund? An emergency fund is a pool of money that you set aside specifically for potential emergencies. This means it’s not used to fund everyday expenses or any goals such as vacations or investing.

As a general rule of thumb, it’s a good idea to have three to six months of expenses put aside for emergencies. You don’t have a fully funded emergency fund to start investing. However, you should have some money set aside before you start.

This is because you want to avoid the situation where you’ve invested money, you then have an emergency but because you don’t have cash, you sell your investments to fund the emergency.

Once your money is invested, you really want to leave that money alone for a significant period of time or until your investment goal is reached. You don’t want to be forced to sell early.

3. Do you have money you’re willing to put aside for a minimum of three to five years? Investing isn’t a short-term game, especially in assets such as real estate or the stock market.

Often, I get asked where people can invest to get a good return in six months or 12 months, and the answer is: if that’s your time horizon, don’t invest in high-growth assets.

This is because things such as real estate and stocks are volatile. That means you have no idea where the market will be in 12 months’ time. No one does.

We do know that over the long term, these asset classes have performed well. By long term, I’m talking decades. So while no one can tell you where the market will be in the short term, there is reason to believe that over the long term, certain assets will continue to perform well.

There’s an old investment saying that goes “it’s not about timing the market, it’s about time in the market”. This means it’s not about when you get in, it’s about how long you stay invested.

4. Do you have some understanding of your risk profile? There are a few different components to your risk profile.

There’s your risk tolerance (how much risk can you stomach emotionally?). There’s your risk capacity (how much risk can you afford to take on financially?). There’s also your risk required (how much risk do you need to take to achieve your financial goals?)

These could all be different for a single individual. For instance, many people are terrified of investing, but it would help them to have some exposure to risk to achieve their financial goals. Others may be keen to start investing, but their financial situation may not be stable enough to warrant taking on that additional risk just yet.

Understanding your risk profile will help you pick an investment option most suitable for your circumstances.

Investing doesn’t start with opening a brokerage account and buying an investment. It starts with laying a strong, stable and secure foundation upon which your portfolio will be built.

Paridhi Jain is the founder of SkilledSmart, which helps adults learn to manage, save and invest their money through financial education courses and classes.

- Advice given in this article is general in nature and is not intended to influence readers’ decisions about investing or financial products. They should always seek their own professional advice that takes into account their own personal circumstances before making any financial decisions.

For expert tips on how to save, invest and make the most of your money, delivered to your inbox every Sunday, sign up for our Real Money newsletter here.

Most Viewed in Money

From our partners

Source: Read Full Article